Mastering Fraud Solution Implementation - The "I Want It All" Trap.

05.08.2026

At first, I thought it was just another payment app. Sleek, branded, maybe with a cashback promo. Turns out, it's the UAE’s biggest leap into digital money. And if you've been seeing that distinctive new 'D' symbol popping up everywhere from shop windows to government websites, you're not alone. The buzz around the 'Digital Dirham' is real, and it’ll definitely change how we chase fraud - for better and for worse.

Before we dive into the implications, let's get our definitions straight. The Digital Dirham is what the experts call a Central Bank Digital Currency (CBDC), essentially the UAE's official currency in digital form. It's a new type of digital money that is issued and guaranteed by the Central Bank of the UAE.

While it will feel familiar to users of wallets like Payit or Klip, the key differences are significant:

It's government-issued money: Unlike digital credits, it's actual government-backed currency.

It's legal tender: Every merchant in the UAE must accept it, period.

It lives on a blockchain: Every transaction is a permanent, tamper-proof record, a receipt that never dies.

And don't worry, unlike volatile cryptocurrencies, the Digital Dirham maintains a rock-solid 1:1 parity with physical dirhams. The full faith and credit of the government backs it, and you won't need a computer science degree to spend it.

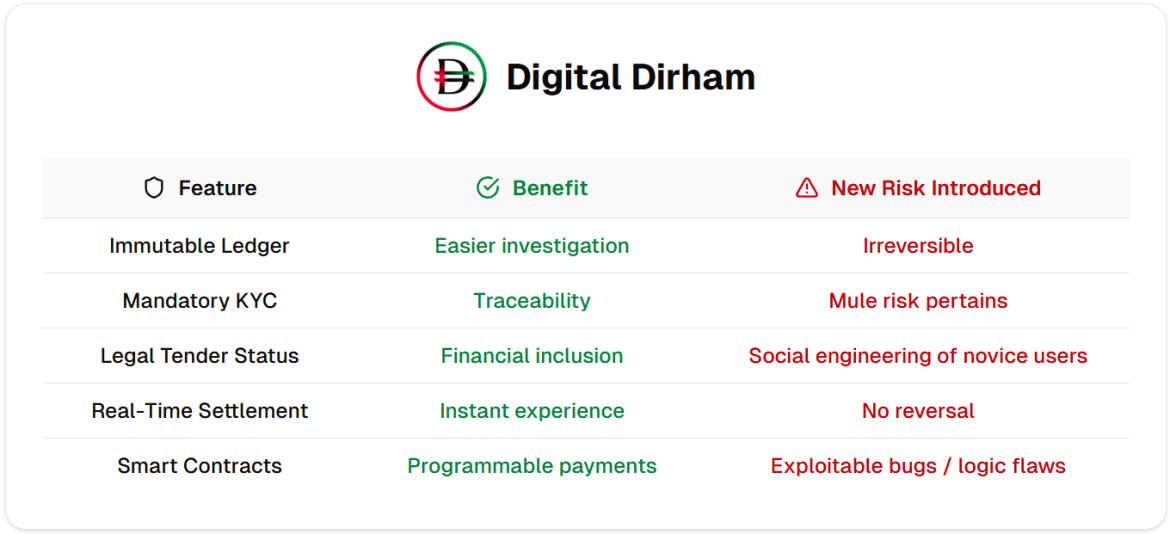

Now, let's examine the key characteristics of the Digital Dirham and what they mean for fraud prevention. Each capability is a double-edged sword - offering genuine benefits while creating new challenges we haven't dealt with before. Understanding these trade-offs is crucial for fraud teams preparing for this new reality.

Remember the last time you tried to trace a cash transaction? Right, you can't, because cash leaves no trail. There's a reason fraudsters (almost) always end their schemes with 'convert to cash and disappear' - it's where our investigation hits a brick wall. The Digital Dirham flips this on its head. Every transaction creates a permanent, unalterable record on the blockchain that authorized parties can access for investigations. A fraudster can't claim "I never received that money" when the ledger shows exactly when, where, and how much was transferred.

This could streamline fraud investigations, provided investigators have the necessary access. Today, when you trace funds from your bank to another institution, you hit a wall. "AED 10,000 sent to account 123-456 at Bank B" is where your visibility ends. To proceed, you need to call Bank B, wait for their response, and then repeat the process if the transaction is transferred to Bank C. With Digital Dirham ledger access, you could theoretically see the complete chain - Wallet A -> Wallet B -> Wallet C -> Merchant D - all in one place, without phone calls or inter-bank delays. The improvement isn't revolutionary, but it's meaningful: faster access and a complete view instead of fragmented systems.

Think the Digital Dirham will kill off the mule account? Not a chance. In fact, fraudsters are already dusting off their playbooks, just with a fresh spin to it.

Every Digital Dirham wallet requires Know Your Customer (KYC) verification, creating a traceable link between transactions and a verified identity. This is a powerful tool, but here's the catch: fraudsters will just find new ways to exploit it. Instead of asking someone to "open a shady bank account," they'll pitch it as "just helping with a new government digital wallet." They'll create fake job postings for "Digital Dirham transaction processors" or use romance scams to trick victims into handling their "official UAE digital currency."

The real advantage isn't in eliminating mules entirely, but in making their lives a whole lot more difficult. When we can trace the complete money trail in real-time, it's not a matter of if we'll find them, but how quickly. The deterrent effect comes from mules knowing their actions are immediately visible to authorities, not from preventing their recruitment entirely.

The Digital Dirham supports smart contracts - essentially programmable money that can execute automatically when certain conditions are met. While smart contracts already exist in wholesale banking, conditional consumer payments are a different story entirely. Think parents giving kids an allowance that only works at certain stores or for specific categories, or business payments that automatically release when delivery is confirmed.

These consumer-facing applications aren't common in today's retail banking world, which means we're entering largely uncharted territory for consumer fraud prevention. While wholesale banking has learned to manage smart contract risks in controlled B2B environments, consumer-scale programmable money creates entirely new attack vectors. What happens when fraudsters figure out how to exploit bugs in consumer smart contracts? We'll be learning these consumer-specific risks as we go.

For every benefit, there's a new risk. The Digital Dirham is no different. We must be prepared for the new vulnerabilities that will arise, because fraudsters will undoubtedly be looking for them.

Remember that feeling of relief when you could freeze a suspicious wire transfer? Get ready to say goodbye to it.

Here’s the double-edged sword of instant settlement. Many traditional banking systems, with their overnight batch processing and “pending” period zones, might seem outdated - but they’ve long served as a safety net for fraud teams (why do you think we have cool-down/activation periods for new beneficiaries?). That delay gives you time to spot shady activity, raise flags, and maybe even call up the receiving bank with a well-timed “freeze that transfer!”

Now enter the realm of Digital Dirham.

This thing settles in real-time. No batch windows. No breathing room. No “hold please” while you frantically pull the alarm. The moment a fraudulent transaction happens, it’s already locked in on the blockchain. Poof - gone. Sound terrifying? Well, yes and no.

It doesn’t mean the funds are lost forever. The Central Bank can reverse transactions, but only under a court order or in clear, proven cases of fraud. This is a critical change: the recovery process shifts from a commercial banking procedure to a courtroom battle. Instead of a quick call to a counterpart at another bank, you're building a case file for a judge.

Here's where the Digital Dirham differs fundamentally from existing wallets: it's legal tender, meaning every merchant in the UAE must accept it. No more "sorry, we don't take that payment method" - if it's Digital Dirham, it's as good as cash.

The financial inclusion benefits are real - domestic workers, laborers, and others who currently operate in cash-only economies can finally access digital financial services without needing traditional bank accounts. But this creates a perfect storm for fraud teams: a large population of new digital payment users who may lack experience with banking products, smartphone security, or common fraud tactics. For fraudsters, this new, tech-novice user base is like a gold rush. These newly onboarded users could become easy targets for social engineering schemes - imagine fraudsters exploiting unfamiliarity with digital wallets to trick workers into sharing access credentials or participating as unwitting mules (the risks related to new and emerging technologies we also touched upon in our WhatFraudsterLike series - here)

Wallet takeover fraud will emerge as an extension of the traditional account takeover. What happens when fraudsters steal Digital Dirham credentials? Unlike bank accounts with multiple authentication layers, compromised wallets allow instant, irreversible fund transfers.

However, the Digital Dirham's design provides some built-in risk mitigation. The wallets are non-interest-bearing (zero interest on the account balance), which naturally discourages people from keeping large amounts in them - most users will likely maintain relatively small balances for daily transactions. Additionally, wallet holding limits are expected to be implemented, further capping potential losses from any single compromise.

The UAE isn't building the Digital Dirham in isolation. They're actively connecting it with other countries' CBDCs through platforms like mBridge, and have already successfully tested cross-border transactions with China and India.

While this creates exciting possibilities for instant international remittances, it also opens new frontiers for cross-border fraud. Currently, international fraud investigations involve lengthy processes. With CBDC integration, fraudsters could potentially move money across borders in seconds while investigators still need weeks to coordinate responses between different regulatory systems. The speed advantage tips heavily toward criminals in the early stages.

Getting Ready for Launch

If you're just starting to think about this now, you're already behind. It's already August 2025. The Digital Dirham is just weeks away, and fraud prevention professionals and participating institutions should be well along with their preparations. The Digital Dirham will require updates to fraud detection systems, revisions and adjustments to investigation procedures, as well as staff training and alignment.

Critically, you'll need to ensure Digital Dirham transactions are captured within your existing anti-fraud solutions to maintain accurate customer behavioral profiles. As customers - especially tech-savvy ones - start using Digital Dirham for daily transactions, you risk losing visibility into meaningful portions of their spending patterns. If these transactions aren't integrated into your current systems, your behavioral models will become incomplete, making existing fraud rules less accurate or even faulty. A customer who suddenly appears to have reduced transaction activity might actually be spending heavily through Digital Dirham - creating false positives and blind spots in your detection capabilities.

The Digital Dirham represents more than just a technological advancement - it's a shift in how money - especially cash transactions - work in a digital world. For those of us fighting fraud, it offers some new tools, but also creates new challenges, some of which we might only learn when we start seeing the first Digital Dirham transactions.

The Digital Dirham won’t kill fraud - but it’ll change where it hides, how it moves, and how fast you need to be to catch it.